Navigating Earnest Money and Contingencies in Washington Real Estate

Navigating a residential transaction in Washington requires a thorough understanding of how earnest money and contract contingencies interact. Earnest money serves as the financial commitment of the buyer. Contingencies act as critical safety valves, allowing the buyer to recover their deposit if specific conditions aren't met. Buyers don't have an automatic right to walk away and reclaim their earnest money. In Washington, contingencies are strictly contractual rights established primarily through Northwest Multiple Listing Service (NWMLS) forms. They aren't automatic statutory guarantees. Understanding these forms and the rules governing trust funds is essential for brokers to protect client interests and maintain their licenses.

Earnest Money Fundamentals in Washington

There's no state-mandated minimum amount for earnest money in Washington. It is entirely a negotiated term. However, the amount carries significant legal implications. Under the liquidated damages safe harbor provision, if a buyer breaches the contract, the seller's retention of earnest money as liquidated damages is generally capped at 5% of the purchase price. Consider a scenario where a buyer offers $100,000 in earnest money on a $1,000,000 home, representing 10% of the purchase price. If the buyer walks away without legal justification, the seller can't simply retain the entire $100,000. The seller is generally limited to $50,000, the 5% cap. Claiming the remaining $50,000 requires litigation to prove actual financial damages exceeding that threshold. Most standard NWMLS agreements explicitly elect the forfeiture of earnest money as the sole remedy for the seller, making the 5% limit an important concept to explain during offer creation.

The timing of the earnest money deposit faces strict regulatory scrutiny. State law requires a broker to deposit earnest money into the firm's trust account or deliver it to the designated closing agent no later than the first banking day following receipt. Buyers frequently wire or deliver earnest money directly to the closing agent. This removes the physical handling of funds from the broker. However, the broker remains responsible for verifying that the deposit occurred according to the timelines in the purchase and sale agreement. When a firm holds the funds, strict trust account segregation applies. Client funds must never be commingled with operating funds.

Promissory Notes as Earnest Money

A buyer may wish to use a promissory note or another noncash instrument as earnest money. State regulations require the broker to provide explicit disclosure to the seller before the offer is accepted. Brokers must advise clients that promissory notes carry significant practical risks. Unlike cash held in a neutral escrow account, a promissory note is an unsecured obligation. If a buyer defaults and refuses to pay, the seller can't simply instruct escrow to release the funds. The seller faces the difficult, delayed process of pursuing legal enforcement in civil court to collect liquidated damages. This scenario commonly arises when a buyer has cash tied up in another sale or illiquid assets. Brokers representing sellers must ensure clients fully understand the greater risk and potential for litigation.

Seller Disclosure vs. Inspection Contingency

It is important to distinguish between the inspection contingency and the statutory seller disclosure statement. Buyers frequently confuse the two, which can have real consequences. The seller disclosure statement is a statutory requirement where the seller answers questions about the property condition to the best of their actual knowledge. For instance, a seller might truthfully disclose no history of roof leaks if the leak is concealed in an unaccessed attic. A buyer may revoke their offer within three days of receiving the statement unless waived. However, the statement isn't a warranty and doesn't replace an independent inspection contingency. It reflects only what the seller actually knows. The inspection contingency empowers the buyer to hire professionals to actively discover unknown conditions.

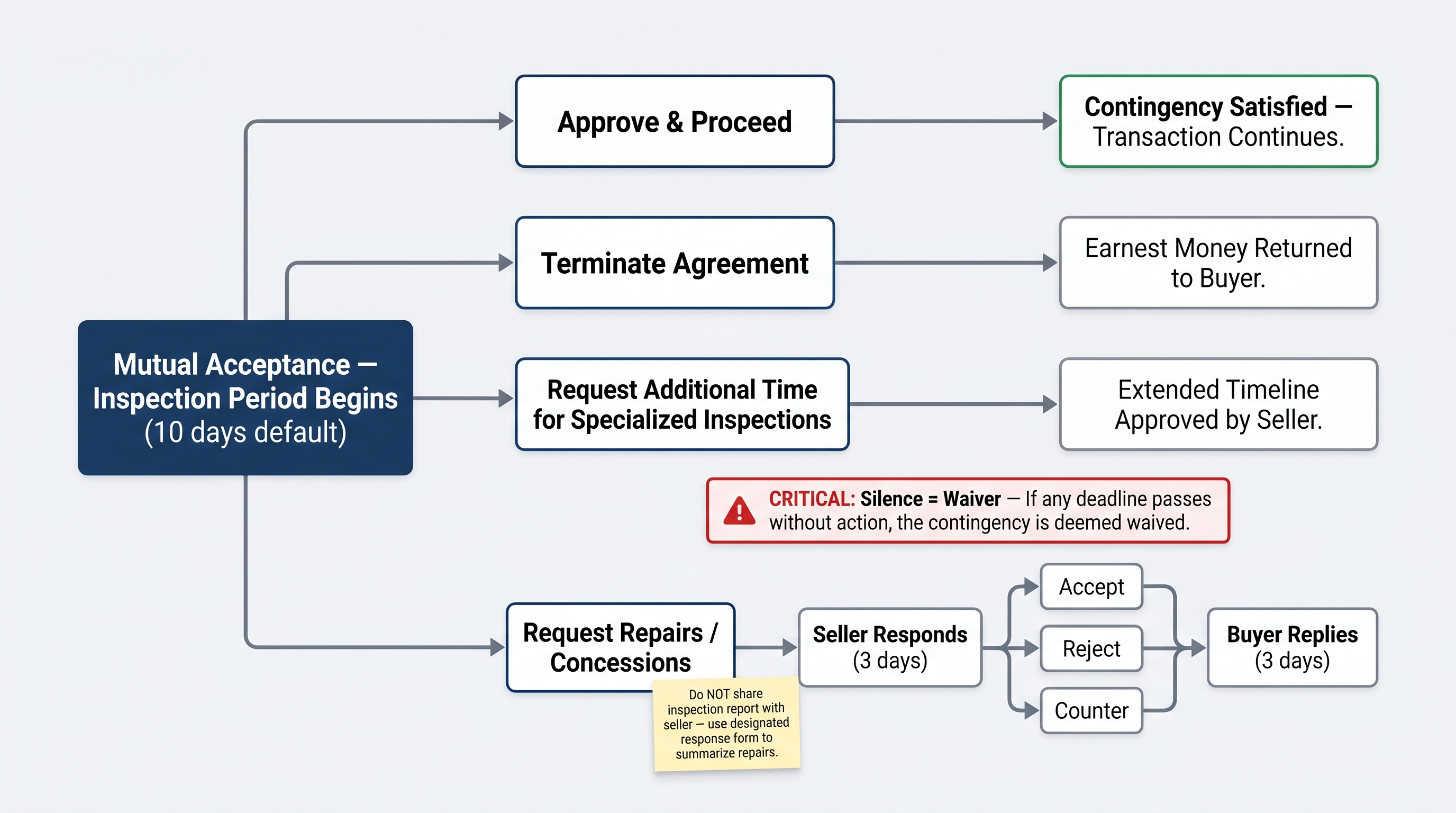

The Inspection Contingency — NWMLS Form 35

The inspection contingency, typically enacted through NWMLS Form 35, is a powerful tool for a Washington buyer. It operates on a subjective satisfaction standard. The buyer may terminate the agreement based on inspection results at their sole discretion without justifying the decision to the seller. The default timeline for the initial inspection period is 10 days. During this window, the buyer must conduct inspections and deliver their response.

Within this period, the buyer can approve the report, terminate the agreement, request additional time, or propose repairs. Brokers must remain attentive to the report-sharing trap. Under standard NWMLS Form 35 provisions, if a buyer or broker shares any portion of the inspection report with the seller without an explicit written request, it may result in a waiver of the inspection contingency. Brokers should verify current form language. The practical risk-management principle is straightforward. Don't send the report to the listing agent simply to justify a repair request. Summarize the requested repairs clearly on the designated response form.

If the buyer requests repairs, the contingency enters a negotiation phase governed by strict default timelines. A fundamental principle of Washington real estate contracts is that silence equals waiver. If any deadline passes without the required action, the contingency is generally deemed waived, binding the buyer to the transaction without the requested repairs.

NWMLS Form 35 Inspection Contingency — Decision Flow and Negotiation Timelines. Note: Always verify current form language and version dates.

The Financing Contingency — NWMLS Form 22A

The financing contingency, structured through NWMLS Form 22A, protects the earnest money of buyers requiring a mortgage. This protection depends on the buyer making a good-faith effort to secure financing. A buyer who deliberately undermines their loan application can't invoke the contingency to recover their earnest money.

A critical aspect of Form 22A is the 20-day lender confirmation requirement. If a buyer is unable to obtain financing and wishes to terminate, they must provide a letter from their lender. This letter must confirm a timely application, sufficient funds to close, and specify the reason for denial. Failure to provide this letter within 20 days of the financing failure generally results in a waiver of the contingency and forfeiture of the earnest money.

Brokers should be familiar with standard provisions within the current NWMLS Form 22A. Standard form language provides that if a buyer explicitly waives the financing contingency, they don't automatically waive the appraisal protection, provided the appropriate provisions remain intact. This feature offers a useful teaching point for buyers competing with cash-like offers who still want a safety net if the home under-appraises. Brokers must verify these provisions against current forms and counsel clients carefully on how waivers affect earnest money.

Enforcing Deadlines: The Notice to Perform

When a buyer fails to meet contractual contingency deadlines, such as failing to apply for a loan on time or neglecting to deposit earnest money, the funds aren't automatically forfeited. The transaction isn't immediately terminated. Sellers must typically issue a formal demand for contractual compliance through a Notice to Perform, such as NWMLS Form 22NS. This notice serves as a strict warning and provides the buyer a defined cure period, often two to three days. If the buyer doesn't perform within that timeframe, the seller acquires the right to unilaterally terminate the agreement and pursue the earnest money. Understanding how to deploy this tool is essential for listing brokers. Without it, a defaulting buyer may tie up the property indefinitely. The Notice to Perform forces the issue and keeps the transaction moving.

Quick-Reference Contingency Timelines

To help brokers manage these strict deadlines, the following table summarizes standard NWMLS default timelines. Always verify the specific terms of each contract.

| Contingency / Action | Standard Default Timeline |

|---|---|

| Initial Inspection Period | 10 days |

| Seller Response to Repair Request | 3 days |

| Buyer Reply to Seller's Response | 3 days |

| Notice of Low Appraisal | 3 days from receipt |

| Seller Response to Low Appraisal | 10 days |

| Financing Failure Lender Letter | 20 days |

Quick-Reference: Standard NWMLS Default Contingency Timelines — Color-coded by deadline urgency. Always verify the specific terms of each contract.

Earnest Money Disputes — When Contingencies Fail

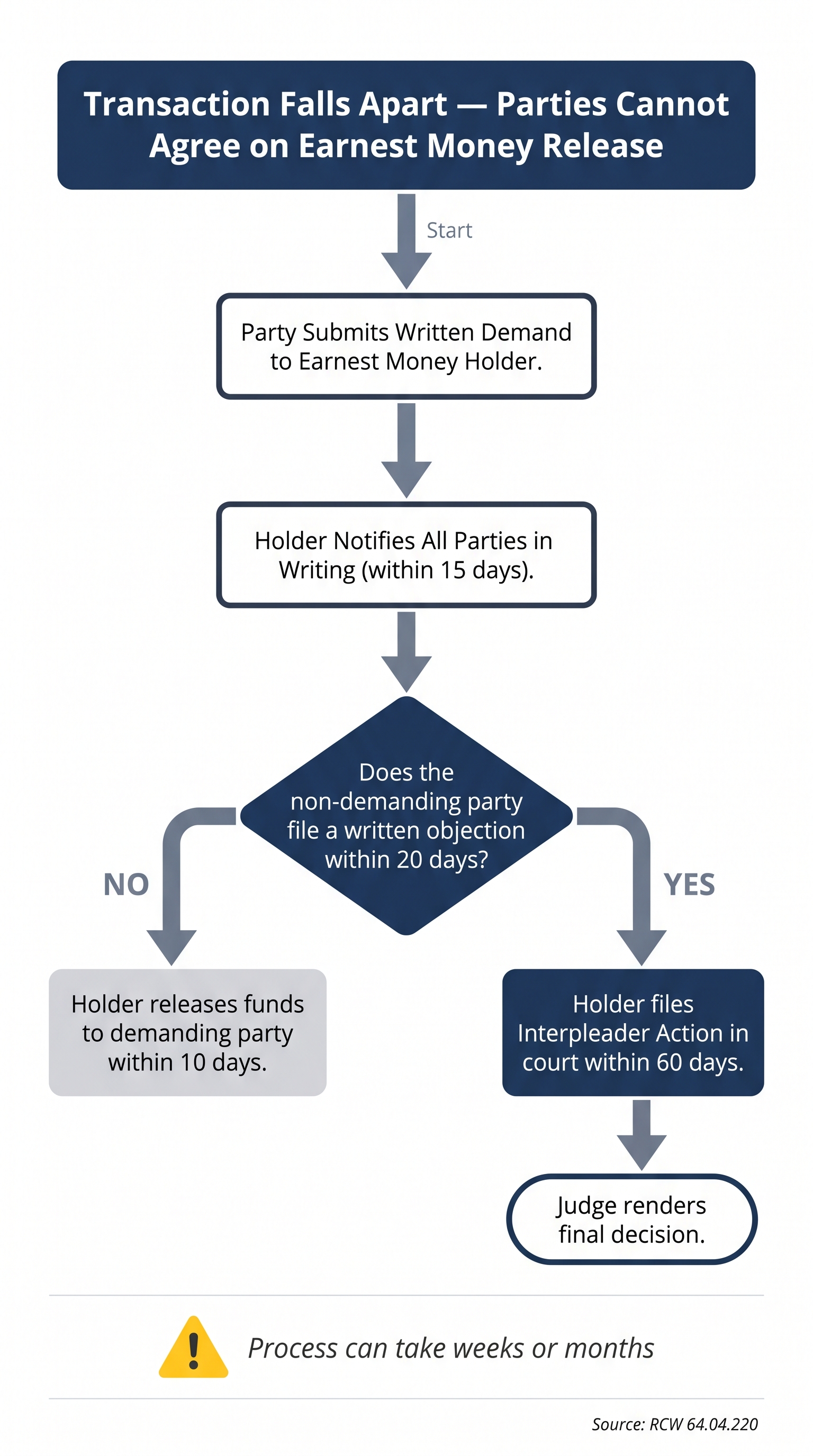

Despite best efforts, transactions sometimes fall apart. State regulations dictate that a broker or closing agent holding trust funds can't disburse disputed earnest money without a written release signed by both parties or a court order.

When parties decline to sign a mutual release, the statutory interpleader process applies. The process begins when a party submits a written demand to the earnest money holder. The holder has 15 days from receipt to notify all other parties in writing. The non-demanding party is given 20 days to file a written objection. If no objection is received, the holder releases the funds to the demanding party within 10 days following the 20-day period. If an objection is filed, the holder must commence an interpleader action in court within 60 days of receiving the objection. A judge then renders the final determination. Brokers should proactively explain this timeline to clients. Disputes resolved through interpleader can take weeks or months.

Washington Earnest Money Dispute Resolution Process (RCW 64.04.220) — Statutory timelines for the interpleader procedure.

Broker Duties and Risk Management

Managing earnest money and tracking deadlines are statutory obligations. Brokers owe strict duties to their clients, including dealing honestly, accounting in a timely manner for all money received, and disclosing all known material facts.

State rules mandate specific document delivery timelines. Brokers must deliver all transaction documents to their managing broker or designated branch manager within two business days of mutual acceptance or receipt. These documents include signed purchase and sale agreements, addenda, and brokerage service contracts. This requirement enables firm leadership to review files for compliance and identify missing earnest money receipts or contingency waivers before they escalate into legal liabilities.

Managing brokers and branch managers carry substantial supervisory responsibilities. They are required to implement policies that ensure the safe handling of client trust funds. They must provide trust account oversight, review transactions, and maintain proper record-keeping practices. Firm leaders must ensure monthly reconciliation of trust account bank records are completed, up to date, and accurate.

Effective risk management requires rigorous systems and consistent follow-through. The Washington State Department of Licensing expects uncompromising compliance. Firms must retain all transaction records for a minimum of three years. These records include earnest money receipts, mutual releases, and contingency addenda. A missing earnest money log or an undocumented contingency waiver can expose a broker or firm to serious disciplinary action.

Conclusion

Mastering the interplay between earnest money and contingencies is a hallmark of a competent Washington real estate professional. By understanding the 5% liquidated damages safe harbor, the strict deadlines embedded in NWMLS forms, and the statutory requirements governing trust funds and dispute resolution, brokers can guide their clients with confidence. Precise adherence to these rules protects the financial interests of the client and safeguards the license of the broker.

Disclaimer: This article is intended for educational purposes only for licensed Washington real estate professionals and does not constitute legal advice. Brokers should consult their managing broker or designated legal counsel for guidance on specific transactions.